Disruption ‘necessary’ to close digital divide, says banker

/ Our Today

administrator

An executive at one of the country’s top three commercial banks has described as “necessary” the disruptions being experienced due to the sudden reliance on digital technologies, because of the COVID-19 pandemic.

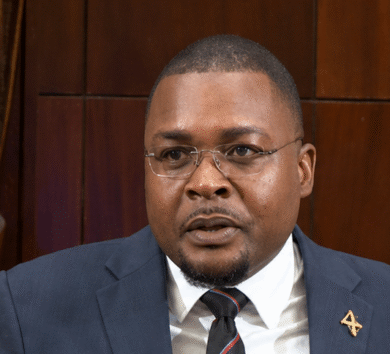

Ricardo Dystant, chief of digital transformation at JN Bank, said the “chaos” right across the country has forced leadership in both the private and public sector to show more interest in closing the digital divide. He was speaking during an online forum entitled ‘Digitisation of Banking: It’s Impact on Jamaican Pensioners and Youth’ organised by final year Accounting and Finance and Management majors at the Portmore Community College in St Catherine.

Pointing to data from the University of Technology’s Professor Paul Golding, Dystant noted that there is a near 50 per cent Internet accessibility gap between rural and urban spaces in Jamaica, with urban areas having 64 per cent access to broadband Internet and rural communities only 36 per cent.

“I do believe that we have all come to recognise that this moment in time is not fleeting. Indeed, it is not a period in our lives which will simply pass by, but, rather, a present that will be our permanent future.”

Ricardo Dystant, chief of digital transformation at JN Bank

The JN Bank chief of digital transformation underscored that the current emphasis on digital adaption is not transitory, and so the issue of Internet availability, and consequently adaption to digital services, has to be taken seriously.

“I do believe that we have all come to recognise that this moment in time is not fleeting. Indeed, it is not a period in our lives which will simply pass by, but, rather, a present that will be our permanent future,” he told the final year of Finance and Management majors.

Those comments were supported by Bashevis Pryce, relationship manager at the National Commercial Bank, who noted that the traditional way of banking has become unsustainable. He said although the digitisation of banking services has been taking place for some time now, the onslaught of COVID-19 has fast-tracked several banks’ thrust to digitise services.

Dystant acknowledged that while there are some policy and deliberate actions being undertaken, efforts need to be ratcheted up to quicken the population’s adaption. Looking specifically at the challenges faced by youth and the elderly, he noted that specific and targeted actions have to be taken to increase the rate of adjustment to the new norm.

Issues facing youth and elderly

He noted for instance that many elderly people do not have the skillset to use online tools; and therefore, tend to be apprehensive about doing digital banking, or using self-service modes of banking. Some are also apprehensive about the security of online banking, but he also noted that affordability of data services is also a problem for the elderly.

“Several are retired and often live alone, and they do not factor in their small pensions or savings, or they simply cannot afford, data services or internet costs, which telecoms companies often package with other services,” Dystant said.

Pryce noted that some also suffer from physical ailments that limit their ability to adapt.

Dystant said although youth tend to be generally more comfortable with online tools and services, they too face some serious challenges that undermine their adaption, as they may not be able to provide all the documents required to open an account.

“There are many who are not exposed to banking services itself and, therefore, do not have access, because of their lack of employment or underemployment,” he said.

He continued: “The unemployment rate among our youth is very high, with some 28 per cent of youth 20- 24 years unemployed, according to the Statistical Institute of Jamaica and 14.4 per cent of those 25-34 years-old without a job.”

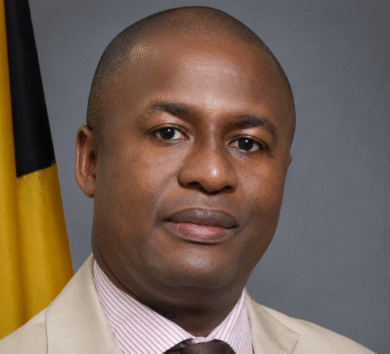

Also speaking at the forum, Richard Campbell, national insurance inspector at the National Insurance Scheme (NIS), added that although the NIS has gone the route of direct deposit to bank accounts instead of preparing cheques for most pensioners, there are some elderly who also don’t have bank accounts, or don’t use banking services, because of poor experiences with banks, or trepidation about using the technology, such as ATMs.

And now that some banks are moving even more vigorously towards technology as a main point of access to services, even repurposing some locations as digital branches, there is concern that the elderly could be further alienated from banking services because of the challenge with digital tools and also the distance some may need to travel to do their banking.

“They will have a disadvantage where online banking is concerned because of internet issues,” Campbell also noted.

“We welcome the digitisation for our pensioners, but there are advantages and also disadvantages. We try at all times to protect them, because they are vulnerable,” Campbell cautioned.

But pointing to efforts by some organisations, including his own to educate the elderly and persons with low levels or no computer or online skills; as well as amendments to the Proceeds of Crime Act to reduce the requirements for opening accounts, Dystant maintained that deliberate and concerted behaviour change and policy initiatives can move people along the adaption curve faster.

“The issues slowing our full adaption are not issues that are insurmountable and, in fact, we have already begun to address them in some ways. We can accomplish the change if we are focused and deliberate about our actions, if we accept that we have come to a point of no return,” Mr Dystant insisted.

“The digital revolution is now. Let us move forward with it.”

Comments