Finance Minister Fayval Williams corrects Julian Robinson’s claim re Debt-to-GDP Ratios

/ Our Today

administrator

Minister of Finance Fayval Williams has moved to correct the recent statement by Julian Robinson, Opposition Spokesperson on Finance, Planning and the Public Service regarding the Debt-to-GDP ratios when the PNP demitted office in February 2016.

Debt-to-GDP Ratio is a metric used to denote the percentage of debt a country has when compared to its Gross Domestic Product (GDP). Debt is the amount of money owed and a country’s GDP is its total value of goods and services produced or made within its borders. High Debt-to-GDP ratios can impact a country’s financial stability and its credit rating.

The Opposition Spokesperson stated that Jamaica’s Debt-to-GDP ratio, when the PNP left office in 2016, was 115%. Williams is reminding the spokesperson and the public of pertinent dates and figures.

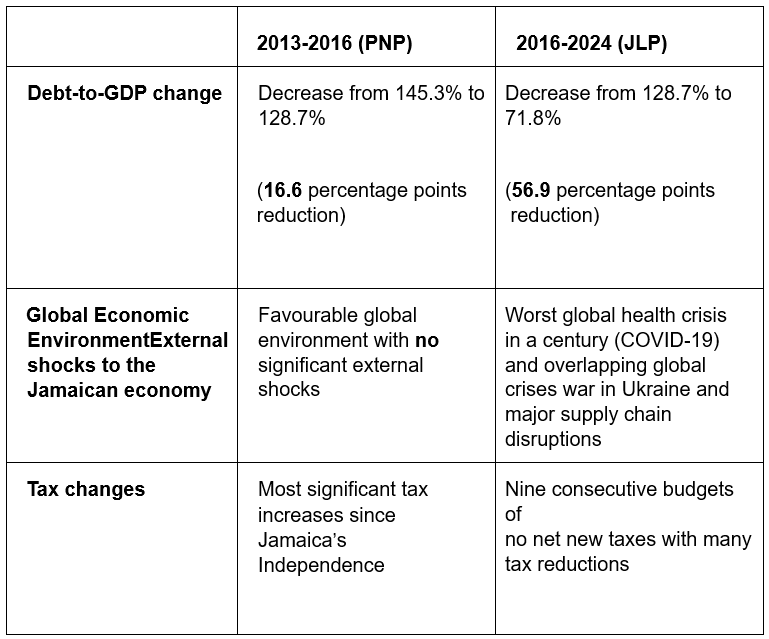

“On December 29, 2011, the PNP won the general election and by the time the second fiscal year ended on March 31, 2013, Jamaica’s Debt-to-GDP ratio had risen to 145.3% from 138.8% at end of March 31, 2012,” Williams said.

The Prime Minister in referencing the Debt-to-GDP, said “no single administration has done it.” He noted in his recent speech in Parliament on Tuesday: “We have cut the debt from 144% of GDP to now about 74% of GDP.”

Williams said it is regrettable that the fundamental point conveyed by the prime minister regarding the Debt-to-GDP ratio being reduced across political administrations was overlooked by the Opposition Spokesperson on Finance.

In addition, the finance minister made reference to the IMF’s Country Report No. 16/181 dated June 2016, following the conclusion of the IMF’s Article IV consultations, which shows that the Debt-to-GDP ratio at the end of March 2016, when the PNP left office was 128.7% and not 115% “as the spokesman incorrectly claims in his statement”.

Recently, in its reviews under the Precautionary and Liquidity Line and the Resilience and Sustainability Facility, the IMF reported a Debt-to-GDP ratio of 71.8% for the recent fiscal year which ended March 31, 2024. This represents 56.9 percentage points of decline, a commendable performance for the present government.

Minister Williams shared the following facts as well:

- The Debt-to-GDP reduction between 2016-2024 under this government, has been far more significant moving from 128.7% to 71.8% as at the end of the fiscal year ended March 31, 2024. This amounts to a reduction of 56.9 percentage points over the period or 7.1 percentage points reduction per year (on average) in the face of extreme global health and natural disaster shocks.

Contrast this with only a 16.6 percentage point reduction achieved by the PNP government during 2013-2016 despite there being no significant external shocks to the economy.

- We must note that during 2016-2024, some of the significant gains achieved were reversed by the impact of COVID-19, the worst global health crisis in a century, as well as the overlapping global crises associated with the war in Ukraine and major global supply chain disruptions. Collectively, the impact of these resulted in the largest external shock that the Jamaican economy has experienced since the country’s independence.

- It is worth noting that during 2013-2016, Jamaicans were burdened with significant tax increases. The 2012/2013 tax package announced was budgeted to raise $19.38 Billion and this was followed by another raft of tax measures in 2013/14 totalling $15.9 Billion. This period saw the most massive tax packages in our independent history.

- For contrast, the Debt-to-GDP reductions during 2016-2024 have been achieved alongside nine (9) consecutive budgets with no net new taxes. In fact, several taxes have been reduced over that period. These include the following:

- The income tax threshold was increased from $592,800 to J$1,700,088, thus reducing the burden of taxes on individuals.

- GCT was reduced from 16.5% to 15%, thus reducing the tax burden on Jamaicans.

- The Turnover Threshold required for registration to pay General Consumption Tax (GCT) was increased from J$3 million to J$10 million, allowing businesses to retain more funds for investments and expansion.

- The rate of Transfer Tax on property was reduced from 5% to 2% and ad valorem Stamp Duty replaced with a flat rate of J$5,000 per document, thus encouraging increased transactions in the property markets.

- The minimum estate value on which transfer tax is levied on a deceased person’s estate was increased from J$100,000 to J$10 million, leaving more money for the families of deceased.

- The Asset Tax payable by non-financial institutions was abolished, providing tax relief to non-financial businesses.

- The Minimum Business Tax of $60,000 per annum was abolished, thus eliminating a financial burden for small businesses.

- The Asset Tax on financial institutions was reduced from 0.25% to 0.125% of taxable assets, resulting in more funds available for lending.

- The pension-relief and age-relief tax exemptions for pensioners were increased from $80,000 to $250,000 each per annum, thus allowing pensioners to receive more income.

- In 2024, taxpayers earning less than $3 million are eligible to receive a reverse income tax credit of $20,000. Again, giving more income to families.

The following table compares the change in Debt-to-GDP between 2013-2016 and 2016-2024 as well as the global economic environment and tax policy changes during those periods:

Minister Williams added: “The Spokesman is entitled to his own opinions but not to his own facts. The data and the facts on the country’s debt-to-GDP reductions are clear and unequivocal. I welcome the opportunity to really set the record straight and to inform the public accordingly.”

Comments