Ambraee Houslin | The Diaspora dollar: Jamaica’s greatest untapped capital market is overseas

/ Our Today

administrator

There is a number that should stop every Jamaican capital markets professional in their tracks: US$12.8 billion.

That is the annual savings potential of the Jamaican diaspora, as estimated by the Caribbean Policy Research Institute (CaPRI). It is not a projection of what the diaspora might one day earn. It is an estimate of what they are saving right now accumulated in bank accounts in Brooklyn, Birmingham, Brampton, and beyond while Jamaica’s capital markets compete for a fraction of it.

For context, Jamaica’s entire GDP sits at approximately US$20 billion. Annual remittances the flows we already count, celebrate, and depend on reached US$3.49 billion in 2025, representing roughly 15 per cent of GDP. And yet, despite that figure representing a genuine economic lifeline, it captures only the most passive expression of what the diaspora is capable of. It is consumption capital money sent to keep households running, to pay school fees, to cover utility bills.

The investment capital, the patient capital, the wealth-building capital that largely stays abroad. But here is the more important argument, the one that has not yet been made with sufficient ambition: mobilising the diaspora dollar is not simply a fundraising exercise. It is the single most catalytic intervention available to Jamaica for deepening its private markets, injecting sustainable liquidity into the JSE, accelerating capital velocity across the economy, and ultimately positioning the island as the financial gateway of a more integrated Caribbean. Done well, it is not just a capital markets story. It is a civilisational one.

The Diaspora we have

The Jamaican diaspora numbers approximately three million people roughly equal to the population living on the island itself. They reside primarily in the United States, where over one million Jamaican-born or – descended individuals live, largely in New York and Florida; the United Kingdom, home to over 400,000, concentrated in London and Birmingham; and Canada, with approximately 300,000, primarily in Toronto.

The Cayman Islands hosts one of the highest per-capita concentrations of Jamaican workers anywhere in the world. This is not a poor diaspora. Jamaicans in North America skew educated and professionally anchored. They are nurses, engineers, lawyers, accountants, and entrepreneurs. They have built wealth in their adopted countries. And critically, they have not forgotten where they are from.

That emotional and cultural attachment is not sentiment. In the language of capital markets, it is a structural advantage. Diaspora investors carry what economists call a “patriotic discount” a willingness to accept slightly lower risk-adjusted returns on home-country investments than they would demand from a purely commercial opportunity, because the act of investing carries meaning beyond the return. Israel leveraged this insight from day one of its statehood. Jamaica has barely begun to.

What we are currently doing with this asset

CaPRI’s research found that diaspora members currently hold approximately US$330 million in Jamaican bank deposits, US$230 million in local business investments, and US$175 million in JSE equities. Against a US$12.8 billion savings pool, these are rounding errors.

The Jamaica Stock Exchange has made genuine efforts as recently as May 2025, the JSE’s Chairman and Managing Director were holding town hall meetings in Philadelphia with diaspora communities. The message was sound. But the infrastructure to convert interest into investment has not kept pace with the aspiration. Diaspora investors face friction at every stage: cumbersome account-opening processes, limited digital platforms, currency conversion costs, and a thin secondary market that constrains exit. A diaspora member in Toronto who wants to invest in Jamaica’s growth story often finds it easier to buy an emerging markets ETF than to open a JSE brokerage account. The opportunity cost of that friction is measured not just in lost capital but in lost compounding returns that should have been building wealth in Jamaica’s capital markets for decades.

The Model that works

The diaspora capital mobilisation playbook has been written. Israel began issuing diaspora bonds in 1951 and has raised over US$46 billion since, using the instrument as the first thread in Israel’s broader integration into international capital markets. India’s India Millennium Deposits of 2000 raised US$5.5 billion within two months. Together, Israel and India have raised between US$35 and US$40 billion through diaspora bond instruments not through charity, but through credible, registered, professionally marketed investment instruments that respected the diaspora’s commercial intelligence while appealing to their emotional connection to home.

Jamaica has the diaspora. It has the macroeconomic credibility over a decade of IMF programme compliance, primary fiscal surpluses, and a debt-to-GDP ratio on a sustained downward trajectory. What it lacks is the instrument, the infrastructure, and the enabling legislative architecture to build both.

The capital velocity argument: Why this is bigger than a bond programme

Here is where most analyses of diaspora capital stop at the bond, the brokerage account, the JSE listing. That framing, while useful, dramatically undersells what is actually at stake. The deeper argument is about capital velocity the speed and frequency with which money circulates through an economy and generates compounding productive activity.

A dollar that sits in a London savings account, earning a modest yield while its owner thinks fondly of Jamaica, has a velocity of zero relative to the Jamaican economy. A dollar invested in a JSE-listed company circulates: it pays salaries, those salaries fund consumption, that consumption sustains businesses, those businesses pay taxes and employ more people, and those employees invest their savings in pension funds that buy more JSE equities. The money moves. It multiplies.

Research across emerging market economies consistently shows investment multipliers running at 1.1 to 2.5 times the initial capital in markets with functioning financial infrastructure. The critical qualifier is “functioning.” In markets where capital cannot easily move from savers to productive enterprises, where the private equity layer is thin, where stock exchange liquidity is shallow, and where there are no intermediate financial vehicles connecting investors to opportunities, the multiplier collapses. Jamaica’s current capital markets architecture limits velocity at two structural chokepoints.

The first: most domestic savings flow either into bank deposits or JSE equities, with almost nothing in between. The private equity layer, the intermediate capital that takes companies from promising to scalable, remains thin. The second: the JSE, historically celebrated for exceptional returns, is constrained by a relatively shallow investor base that limits price discovery and makes it difficult for institutional participants to build or exit positions at scale without moving the market.

Diaspora capital, properly structured and channelled, addresses both chokepoints simultaneously.

Deepening private markets: The diaspora as the missing limited partner

Jamaica’s private equity ecosystem faces a fundamental structural challenge: it cannot raise enough domestic capital to populate meaningful fund sizes. Vehicles like JASMEF are beginning to build track records, but a private equity fund that cannot attract committed capital from institutional limited partners cannot deploy at scale, build portfolio diversification, or attract the calibre of fund management talent that generates superior returns.

The Jamaican diaspora is structurally the ideal limited partner for this asset class. Private equity requires patient capital committed for seven to ten years, absorbing early-stage volatility, waiting for compounding to work. Diaspora capital deployed by individuals who have built wealth over careers spanning decades, investing at least partly from connection to home rather than pure return optimisation, is among the most naturally patient capital in the world.

Structured diaspora-led private equity vehicles, potentially seeded with government or DFI anchor commitments to establish credibility, then marketed to the diaspora through dedicated investor relations infrastructure, could mobilise hundreds of millions into Jamaica’s private capital markets. The knock-on effects are compounding. Private equity-backed companies that achieve institutional governance standards become viable IPO candidates.

Those IPOs list on the JSE, adding depth. More listed companies attract more investors. More investors create more liquidity. More liquidity lowers the cost of capital for every company in the market. The entire system becomes self-reinforcing but only if the private capital layer is sufficiently capitalised to generate the pipeline.

The diaspora is the missing limited partner. Recognising this is the first step. Building the enabling legislation is the second.

JSE liquidity: The diaspora as the missing investor base

The JSE remains a relatively thinly traded market. Daily volumes often reflect a narrow investor base cycling in and out of a limited number of highly liquid counters. For the exchange to function as a genuine price-discovery mechanism, to attract international institutional investors, and to enable companies to raise material amounts of capital at competitive costs, it needs a substantially deeper and more diverse investor base.

Three million diaspora members, many of them financially sophisticated, represent precisely that investor base. They already own homes, hold retirement accounts, and participate in capital markets in their countries of residence. What they lack is convenient, trustworthy access to the JSE.

Beyond retail participation, diaspora-funded private equity and unit trust vehicles — if listed on the JSE — would add a new category of institutional-quality instruments to the exchange. A listed fund that diaspora members can buy and sell provides an exit pathway that direct equity investment does not, reducing the illiquidity premium that currently discourages diaspora capital from entering the market at all.

The Caribbean flywheel: From Jamaica to regional integration

Now extend the argument one level further.

The Caribbean has discussed regional capital market integration for decades. The Barbados Securities Exchange, the JSE, and the Trinidad and Tobago Stock Exchange have maintained cross-listing arrangements since 1991. Yet CARICOM officials themselves have acknowledged openly that Caribbean exchanges are “essentially lacking liquidity because of their smallness,” with price differentials of cross-listed stocks averaging five per cent a textbook indicator of a fragmented, inefficient market.

The fundamental constraint is not regulatory will. It is capital mass. No individual Caribbean jurisdiction, acting alone, can solve this. But the Jamaican diaspora, as a capital base, is large enough to shift the regional equation.

Here is the strategic proposition: if Jamaica mobilises even a meaningful fraction of its diaspora capital into a well-structured investment ecosystem, private equity vehicles, JSE-listed funds, sovereign diaspora bonds,and direct equities and if that ecosystem is architected from inception for regional scalability, it does not merely deepen Jamaica’s capital markets. It creates the anchor liquidity pool around which a genuinely integrated Caribbean capital market can form.

Jamaica, by virtue of its English-language dominance, its macroeconomic credibility, its relatively sophisticated capital markets infrastructure, and the sheer size of its diaspora, is the natural candidate to serve as the financial hub of the Caribbean Single Market. A JSE with a deeper investor base, driven partly by diaspora capital, becomes the natural primary listing venue for regional companies. Caribbean companies listed in Kingston, traded by Jamaican diaspora investors in New York and London, suddenly have access to a genuinely international investor base. That combination of local knowledge, diaspora reach, and regional ambition is the architecture of a Caribbean financial centre.

The legislative architecture: What government must build

This is where vision becomes policy and where Jamaica’s legislative record must be both honestly assessed and decisively extended. The good news is that the existing regulatory framework is a credible foundation.

The harder news is that it was not designed with diaspora capital mobilisation in mind, and meaningful gaps remain. Closing them requires deliberate legislative action across five interconnected domains.

I. A Jamaica Diaspora Investment Act

The single most important legislative action Jamaica can take is the enactment of a standalone Jamaica Diaspora Investment Act a dedicated statutory framework governing the creation, issuance, marketing, and ongoing administration of diaspora-targeted investment instruments.

This Act would need to accomplish several things that current law does not adequately address: Define the diaspora investor class.

Jamaica’s Securities Act currently makes no formal distinction between a domestic retail investor, a foreign institutional investor, and an overseas Jamaican national. A Diaspora Investment Act would create a recognised legal category the Non-Resident Jamaican Investor (NRJI) defined by nationality, ancestry, or demonstrated cultural connection to Jamaica, regardless of current country of residence. This classification is foundational: it enables the creation of instruments targeted exclusively at this group, the marketing of those instruments in foreign jurisdictions under bilateral recognition agreements, and the application of tailored regulatory standards. Authorise sovereign diaspora bond issuance.

While the Government of Jamaica can issue debt instruments under existing law, there is no specific statutory provision for the creation of diaspora bonds registered, multi-currency, internationally distributed sovereign instruments designed for non-resident Jamaican investors. The Act would provide that specific authority, including the mandate for the Ministry of Finance to establish a Diaspora Bond Programme, appoint a programme manager, set prospectus disclosure standards consistent with both Jamaican and international securities law, and require that proceeds be directed to a ring-fenced Diaspora Development Fund with transparent, publicly reported project allocation.

Require SEC registration equivalence. One of the clearest lessons from Israel and India is that registration with the securities regulator of the investor’s country of residence is non-negotiable for scale. Israel Bonds are registered with the US Securities and Exchange Commission. India’s instruments were distributed through international banking networks with the necessary regulatory authorisations. The Diaspora Investment Act should mandate that any diaspora bond offered to US-resident Jamaicans be registered with the SEC as a foreign sovereign debt instrument, and should empower the Minister of Finance to enter into mutual recognition agreements with the FCA in the United Kingdom and equivalent bodies in Canada to enable compliant marketing in those jurisdictions. This is not merely a compliance matter it is a credibility signal to the investor.

II. Amendments to the Securities Act: Digital Onboarding and Remote Access

The existing Securities Act and its accompanying FSC regulations were drafted in an era of physical presence. The requirement for in-person customer due diligence, the paper-based account opening processes that persist across many Jamaican broker-dealers, and the absence of a regulatory framework for fully digital KYC verification are structural barriers to diaspora participation that no amount of marketing can overcome.

Required amendments include:

- Statutory recognition of digital KYC. The FSC should be empowered through amendment to the Securities Act or through new regulations under the FSC Act to prescribe digital identity verification standards for Non-Resident Jamaican Investors that are equivalent to, but not dependent upon, physical presence. This means formally authorising video-based verification, biometric document authentication, and third-party identity verification services that meet FATF standards. India, the United Kingdom, Canada, and the United States all have established digital KYC frameworks. Jamaica should adopt a mutual recognition approach: if a diaspora investor has been KYC-verified to the standard of their country of residence’s financial services regulator, that verification should be accepted by Jamaican broker-dealers without duplication.

- Non-resident account frameworks. The FSC regulations should be amended to create a formal Non-Resident Investor Account (NRIA) category a standardised account structure that allows diaspora investors to hold JSE securities in USD or GBP denomination, receive dividends in foreign currency, and repatriate proceeds without triggering onerous foreign exchange approval processes. The Bank of Jamaica’s existing foreign exchange guidelines would need corresponding amendment to designate NRIA accounts as a streamlined foreign currency pathway.

- Remote prospectus distribution. The current FSC issuer guidelines require physical distribution infrastructure that is effectively inaccessible to overseas investors. Amendments should explicitly permit fully digital prospectus delivery, digital subscription applications, and electronic settlement for NRJI-category investors, bringing Jamaican securities law into alignment with international standard practice.

III. Amendments to the Income Tax Act — The Investment Incentive Stack

Tax treatment is the second most important lever after access infrastructure. Jamaica has taken a significant positive step: effective April 1, 2025, the withholding tax on dividends paid to non-resident individual shareholders was reduced from 25 per cent to 15 per cent, harmonising the rate with that applied to resident shareholders and removing a deterrent that had long suppressed overseas investment in Jamaican equities.

This is the right direction. But it is not sufficient on its own. A comprehensive diaspora investment incentive stack requires additional legislative action:

Withholding tax exemption on diaspora bond interest. The Income Tax Act should be amended to exempt from Jamaican withholding tax all interest income earned by NRJIs on qualifying diaspora bond instruments. This mirrors the approach taken by India, where the State Bank of India’s diaspora bond interest was expressly exempt from Indian income tax for NRI investors. The exemption sends a clear signal that Jamaica is not merely opening its capital markets to the diaspora but actively incentivising participation. The fiscal cost of the exemption applied to a pool of new, incremental capital that would not otherwise be invested in Jamaica is de minimis relative to the economic activity the underlying investment generates.

Capital gains treatment clarification for non-residents. Jamaica does not impose capital gains tax a significant structural advantage for JSE investors. However, the existing Income Tax Act does not clearly articulate this benefit for non-resident investors in a way that is readily accessible or understood by diaspora investors receiving advice from foreign financial professionals. A specific provision clarifying that NRJIs are not subject to any Jamaican tax on capital gains arising from JSE-listed investments would remove a common source of investor uncertainty and would be a straightforward amendment with no revenue cost.

Tax incentive for diaspora-targeted private equity funds. The Income Tax Act should be amended to provide a specific incentive for FSC-registered investment vehicles that meet a “Diaspora Capital” designation meaning at least 40 per cent of their committed capital is sourced from NRJI investors. Such vehicles should be eligible for a reduced income tax rate on fund-level income (or pass-through treatment), and their NRJI investors should receive a tax credit on dividends received from designated Diaspora Capital Funds. This mirrors the structure of the Junior Market tax incentive that has been instrumental in driving JSE listing activity, and extends the same principle to the private capital layer.

IV. A National Diaspora Investment Registry Act

One of the persistent failures of diaspora engagement programmes globally is the absence of a formal, maintained registry of diaspora investors a structured database that allows the government and private sector to communicate investment opportunities, distribute prospectuses, report on programme performance, and build the ongoing relationship that converts a one-time diaspora bond subscriber into a long-term Jamaican capital markets participant.

A National Diaspora Investment Registry Act would establish:

A formal diaspora investor registry, maintained by a designated government entity (most logically the Ministry of Foreign Affairs and Foreign Trade, working with the Ministry of Finance), into which NRJIs may voluntarily register their investment interest, country of residence, investment capacity, and areas of sectoral focus.

Privacy and data protection obligations consistent with GDPR (relevant for UK-based diaspora), Canada’s PIPEDA, and equivalent US standards essential for the registry to be legally operable across the three principal diaspora markets.Investor relations obligations for issuers who market instruments to registered NRJIs: standardised quarterly reporting, project progress disclosure, and return attribution reporting that allows diaspora investors to track the real-world impact of their capital.

The registry is not merely administrative. It is the intelligence infrastructure that allows Jamaica to understand its diaspora investor base, tailor instruments to their needs, and communicate with them at scale. Without it, every diaspora capital mobilisation effort remains an exercise in shouting into the void.

V. A CARICOM Diaspora Capital Compact: The Regional Treaty Layer

The final and most architecturally ambitious legislative requirement is not purely domestic: it is a regional agreement. Jamaica should lead the negotiation, under the CSME framework, of a CARICOM Diaspora Capital Compact a binding regional treaty that harmonises the regulatory treatment of diaspora investors across the English-speaking Caribbean, enables cross-border passporting of diaspora investment instruments, and establishes a joint Caribbean Diaspora Bond Programme jointly marketed to the collective Caribbean diaspora.

This compact would require:

Regulatory harmonisation. Participating CARICOM states would agree to mutual recognition of their respective diaspora investor classification frameworks, KYC standards, and securities registration requirements, enabling a Barbadian diaspora investor in the UK to invest in a Jamaican-issued instrument, or a Trinidadian diaspora fund to list on the JSE, without duplicating regulatory compliance across jurisdictions.

A joint Caribbean Diaspora Bond. A jointly issued, CARICOM-backed diaspora bond with proceeds allocated proportionally to infrastructure projects across participating states would have a total addressable market an order of magnitude larger than any single-country instrument. The collective Caribbean diaspora across the English-speaking region represents a combined financial capability that, properly organised, is competitive with small sovereign wealth funds.

A Caribbean Investor Passport. An optional, voluntary status granted by a CARICOM member state to any Caribbean-heritage individual resident abroad that confers standardised investor rights across all CARICOM capital markets, regardless of which member state’s exchange they choose to invest through. This is the capital markets equivalent of the free movement of persons agenda, and it is the missing piece that would make the Caribbean Single Market meaningful for its diaspora.

The Accountability Question

Any serious discussion of diaspora capital mobilisation must address the trust deficit directly, because ignoring it is the surest path to failure. Ethiopia’s diaspora bond efforts in 2008 and 2011 failed not because the diaspora lacked capital or affection for home, but because investors lacked confidence in government transparency. Diaspora bonds are accountability instruments. They only work when the issuing country has earned the right to make the ask and continues to deserve it through consistent, verifiable disclosure.

Jamaica has largely earned that right. But the legislation proposed above must be accompanied by an institutional commitment to investor-grade accountability: ring-fenced bond proceeds that cannot be raided for general budget purposes, independent project oversight, and published annual reports that show diaspora investors in plain language, in the currency they hold exactly what their money built and what return it generated.

CaPRI’s research found that trust is the single most significant barrier to diaspora investment. Not returns. Not access. Not knowledge. Trust. The legislative architecture matters enormously, but it is only as valuable as the institutional culture that implements it.

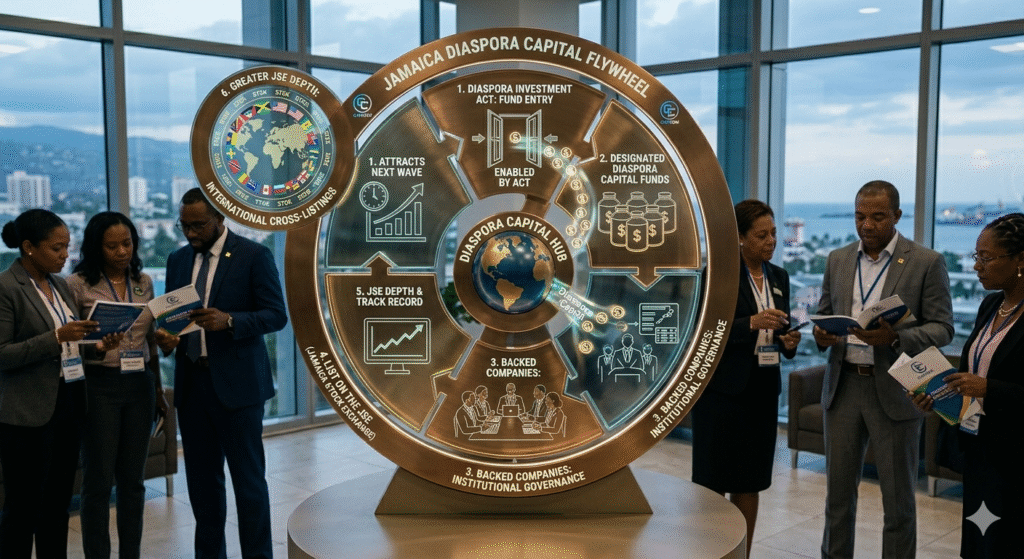

The Flywheel in Motion

Let us trace the full chain of consequences if Jamaica executes this with genuine ambition. Diaspora capital, enabled by the Diaspora Investment Act, enters the private equity ecosystem through designated Diaspora Capital Funds. Those funds back companies that achieve institutional governance standards. Those companies list on the JSE adding depth to the exchange and generating the track record that attracts the next wave of diaspora capital. Greater JSE depth attracts international cross-listings.

Regional companies list in Kingston because it offers the deepest, most accessible investor base in the Caribbean. The JSE becomes the anchor exchange for a more integrated CARICOM capital market. Capital circulates not just within Jamaica but across the region. Companies in Barbados raise equity in Kingston.

Infrastructure projects in Guyana issue bonds accessible to Jamaican diaspora investors in Florida. The velocity of capital across the entire Caribbean economy accelerates. This is the flywheel. It starts with a diaspora dollar that currently sits in a savings account in Brooklyn. It ends if we build the right architecture with a Caribbean capital market that is genuinely integrated, genuinely deep, and genuinely capable of financing the region’s own development at the pace the opportunity demands.

The Larger Stakes

Jamaica’s development challenge has always been a capital allocation challenge more than a resource challenge. The island has talent, infrastructure, geographic position, macroeconomic discipline, and a globally recognised brand. What it has consistently lacked is the depth and breadth of domestic capital markets to fund its own growth story at the pace and scale the opportunity warrants.

The Jamaican diaspora represents the most natural solution to that problem that exists anywhere in the world. Three million people, earning in hard currency, saving at scale, emotionally invested in Jamaica’s success, and currently underserved by the financial architecture that should be connecting their capital to the island’s growth.

Five legislative pillars the Diaspora Investment Act, the Securities Act digital access amendments, the Income Tax Act incentive stack, the Diaspora Investment Registry Act, and the CARICOM Diaspora Capital Compact are not a wish list. They are a precise, sequenced, executable legislative programme that can be developed in consultation with the FSC, the Bank of Jamaica, the Ministry of Finance, and international capital markets advisors, and enacted within a single parliamentary term.

The diaspora dollar is waiting. The flywheel is ready to turn. The legislation is the hand that starts it.

Ambraee Houslin is a private equity strategist with a strong background in economics and statistics. He has extensive experience in investment banking, corporate finance, and investment research across Jamaica and the Caribbean region. His core expertise includes mergers and acquisitions, capital structuring, and executing complex transactions that drive growth and value creation. Ambraee has led and supported deals spanning strategic acquisitions, private credit facilities, and post-transaction integration strategies for high-impact sectors.

Comments